Land Betterment Charge

Last updated 12 March 2026

With effect from 1 August 2022, a new Land Betterment Charge (LBC) has replaced Differential Premium, Development Charge (DC) and Temporary Development Levy (TDL), which were previously administered by the Singapore Land Authority (SLA) and Urban Redevelopment Authority (URA) respectively. The LBC is a tax on the increase in value of land arising from a chargeable consent (e.g. planning permission) given in relation to a development of any land.

Landowners seeking to develop their sites need not make a separate application to SLA for the payment of LBC once a planning application or plan lodgment for an authorised development has been submitted to URA. If the proposed development results in an increase in land value, SLA will follow up directly with the taxable person by issuing a Liability Order (LO) stating the LBC payable. Payment must be made to SLA within 1 month from the date of the LO. This will apply to all planning permissions, plan lodgement and variation of restrictive covenants granted on or after 1 August 2022.

The principles for computing LBC follow the previous DP and DC systems, known as the Table of Rates method. LBC will be computed based on the difference between the value of the post-chargeable valuation and pre-chargeable valuation. Post-chargeable valuation is the value derived from the variation of the relevant restrictive covenant, or the proposed use(s) and intensity in URA’s planning permission or plan lodgement. Pre-chargeable valuation is the value derived from the restrictive covenants in the State title or the last authorised/approved development. The historical Master Plans 1958/1980/2003 will continue to be taken into account in the determination of pre-chargeable valuation, where applicable.

For more information, please refer to this circular dated 5 July 2022 and the attached documents.

LBC Estimator

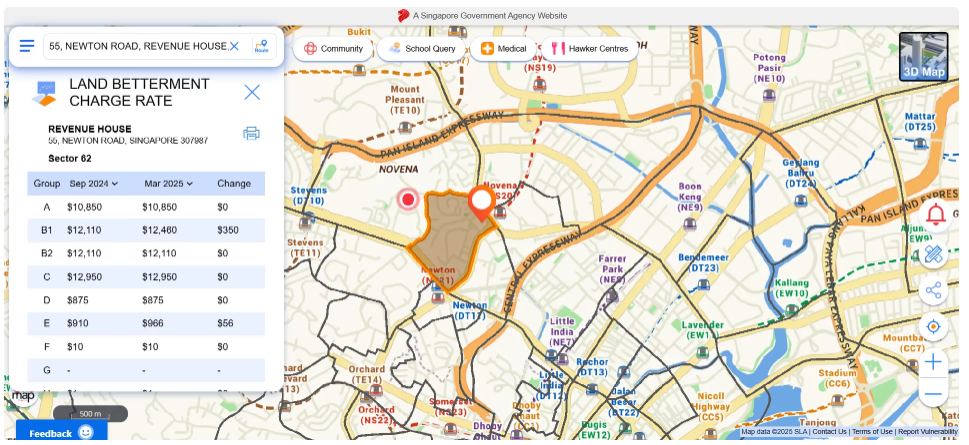

As the LBC amount is an important consideration in business decisions, SLA has taken steps to streamline the LBC process and provide businesses with greater upfront clarity on the LBC amount through an online LBC Estimator. The LBC Estimator enables users to independently estimate the LBC payable for selected development proposals.

Read our #SLAExplains article on the LBC.

LBC Circulars

S/No. | Date | LBC Circulars |

|---|---|---|

1 | 2 July 2022 | |

2 | 29 August 2025 | ENHANCED CLARITY ON LAND BETTERMENT CHARGE FOR SOLAR DEVELOPMENTS |

3 | 27 February 2026 |

Table of Rates 2022

Month/Year | Sector Maps | Use Groups | Table of Rates |

March 2022 | |||

September 2022 | Land Betterment Charge Table of Rates as of 23 September 2022 |

Table of Rates 2023

Month/Year | Sector Maps | Use Groups | Table of Rates |

March 2023 | |||

September 2023 | Land Betterment Charge Table of Rates as of 1 September 2023 |

Table of Rates 2024

Month/Year | Sector Maps | Use Groups | Table of Rates |

March 2024 | |||

September 2024 | Land Betterment Charge Table of Rates as of 1 September 2024 |

Table of Rates 2025

Month/Year | Sector Maps | Use Groups | Table of Rates |

March 2025 | |||

September 2025 | Land Betterment Charge Table of Rates as of 1 September 2025 |

Table of Rates 2026

Month/Year | Sector Maps | Use Groups | Table of Rates |

March 2026 |

From 1 March 2024, the LBC Rates for all Use Groups from September 2022 to March 2026 will be available on OneMap. Members of the public can check the LBC rates for the respective geographical sectors on OneMap.

For use in determination of pre-chargeable value for safeguarded historical base line (where applicable)

Processing Fee

A fee of $1,100 will be collected for an application to update the Baseline database, and this will be payable together with the LBC when the liability order is issued.

Option for Spot Valuation

In cases where there is no suitable or comparable use group for assessment, the Valuation method will apply. Taxable persons may also elect to use the Valuation method, which is irrevocable, in lieu of the Table of Rates method by using this form.

Application for the Election of Valuation Method

Receiving a Liability Order

Every liability order will include details such as (i) the amount of LBC payable; (ii) the name of the taxable person(s) (and apportionment, if any); and (iii) the methods by which payment for LBC can be made. Upon receipt of a liability order, the LBC payable by a taxable person is due to SLA at the end of one month. Once LBC has been paid in full, the liability order will cease to have effect.

Forms

Assumption of Liability Notice

A person who wishes to assume liability to pay any LBC for a chargeable consent may inform SLA by using this form.

Application for Assumption of Liability

Deferment Determination

A charitable institution which is using the land wholly or mainly for charitable purposes may apply to SLA for a deferment to pay LBC by using this form.

Application for Deferment Determination

Transfer of Deferred Liability

A taxable person whose liability to pay any LBC is deferred may apply to transfer his deferred liability to another person by using this form.

Application for Notice of Transfer of Deferred Liability

Evidentiary Certificate

An owner or prospective owner of a land may apply for a certificate in relation to matters mentioned in section 55(1) of the Land Betterment Charge Act by using this form.